Budget 2015-2016 to boost growth; FM ignores gem and jewellery industry.

Over the last decade, as the earnings and wealth of Indian consumers have soared, attitudes towards luxury have begun to change and the demand for high value goods and services has begun to shoot up significantly. Young Indians do not frown over conspicuous consumption unlike their forefathers; riches are being acquired without embarrassment and luxury labels are being flaunted with confidence and pride.%%

Recent studies indicate that this is only the tip of the iceberg, and the demand for luxury goods and services is poised to explode in terms of both volume and geographical spread over the next few years. %%

While this is clearly exciting news for jewellers in India, it also brings to the forefront a contradiction that they have always faced – jewellery is the only high value product that is actually priced and sold like a commodity rather than a luxury item. %%

The ‘cost of materials plus making charges formula’ that is predominant throughout the country squeezes margins, and impacts branding, marketing, sales and service and all the other related activities that are necessary for jewellery to be perceived and purchased as a luxury item. %%

Stephen Rego analyses some aspects of the Indian luxury market and the emerging luxury consumer, and discusses some pertinent questions about what jewellers need to do to tap the enormous potential in this sphere. %%

The last few months have brought good news for the Indian jewellery industry -- in the form of three major studies related to the luxury market. %%

The first was the Luxury Goods Worldwide Market Study, by global business and strategy consulting firm Bain & Company, which reported that the global luxury market, severely impacted during the last two years by the financial crisis was now showing signs of recovery. %%

The report predicted a 10% rise in sales in this sector to € 168 bn this year and noted that this would continue into 2011, by when the global luxury-goods sector is expected to return to pre-crisis levels. In April this year, Bain had projected a 4% growth rate, but revised this upward by October due to stronger-than-expected economic growth. %%

Part of this growth would be boosted by favourable exchange rates, but the role of shoppers from the two booming Asian economies – India and China – would also be significant. Interestingly Bain & Co’s report saw the impact of these two countries is taking place at two levels – strong growth of domestic demand for luxury goods in both countries and the “increasing flows of Asian and Chinese shoppers to Europeâ€.

According to the U.S. consultancy the overall rise in demand in the luxury sector could be attributed to an increase in international travel, a boom in e-commerce and a good performance of the retail sector. Bain & Co also forecast that though the pace of growth should slow to between 3% and 5% to € 173 to 176 billion, it would have crossed the pre-crisis peak of € 170 billion registered in 2007 by then. %%

On a global scale, Bain identified the emerging Asian markets, particularly China, which at present is the fastest-growing luxury market, as being the drivers of this surge. While this may sound positive for the Indian luxury industry, a closer look reveals that the picture is not so rosy. %%

Though in terms of absolute numbers, India with its billion plus population is almost as big a market as China, in the luxury sector it lags far behind. The report estimates the size of the luxury market at € 800 million, and projects a healthy 4-5% growth during the year. %%

But these figures are not so impressive when compared to our Asian neighbour, China, with a market size of € 9.2 billion and massive 30% year-on-year growth in 2008, 20% in 2009, and a predicted 30% in 2010. %%

Another recently released document, The World Wealth Report 2010 by Capgemini and Merrill Lynch, however analyses the potential of the Indian luxury market from a slightly different perspective – that of the numbers of HNIs (High Net Worth Individuals). %%

It has some startling facts that confirm what many analysts have been suggesting – that Asia Pacific is the growth engine of the coming decade. The report notes that at 3 million the numbers of HNIs in the Asia-Pacific region now equals that of Europe and that the wealth generated by individuals there is now larger than that of Europe. The total wealth of this segment in the Asia Pacific now stands at $9.7 trillion (up 30.9% over the previous year), inching ahead of the $9.5 trillion held by Europe's HNIs. %%

The surge is particularly marked in India — where the population of HNIs (having minimum investible assets of USD 1mn) surged 50.9% to 1,26,700 in 2009 from 84,000 the previous year. This was significantly faster than the 20.4% and 30.4% growth in the number of HNIs in the world and Asia-Pacific region respectively, and represents a huge 81% increase when compared to the absolute numbers in 2005.

Releasing the report, Pradeep Dokania, chairman, Merrill Lynch global wealth management, India, noted, "The rebound in HNI numbers is highly correlated to the strong recovery in stock prices and strong outlook for India's underlying economy." %%

Significantly, wealth generation in India is seen both at the very high end and the upper middle class segments and is expected to continue to register strong growth in the coming years. %%

Other reports not directly related to the luxury segment confirm this assessment. For example, according to NCAER (2009) survey - India has 46.7 million high income households1 as compared to 41 million in the low income category. Middle income households surged to 140.7 million (300 m adults) out of the total of 228.4 Indian million families at the end of 2009-10. (Average 5 persons per household – 2 adults). %%

THIS IS A FOOTNOTE( Households earning less than Rs. 40,000 per annum (at 2001-02 prices) are dubbed as low income, whereas those with earnings over Rs. 1.80 lakh fall in the high income category. Those earning between Rs. 45,000-Rs 1.80 lakh per annum are considered middle income households.) %%

Further, a study by the McKinsey Global Institute titled The Bird of Gold: The Rise of India’s Consumer Market suggests that if India continues its growth, the average household disposable incomes will more than double in the next 15 years from Rs.1,20,000 in 2010 to Rs.3,00,000 in 2025. %%

Returning to the luxury market, the third recently released report referred to earlier was a study entitled Luxury in India: Charming the Snakes and Scaling the Ladders prepared and published by Confederation of Indian Industry (CII) and A T Kearney. The report was released at the second edition of the CII’s Luxury Goods Forum held in Delhi on October 7, 2010 as part of the Commonwealth Games Business Forum. %%

The report estimates that in 2009 India's luxury industry including products, services and assets stood at $4.76 billion. Though this is small compared to global standards, the figure is expected to grow three times and touch $14.7 billion by 2015. %%

The study believes that there is a massive ‘latent demand’ as growth of the luxury industry has been constrained by both supply and demand side factors in the past, but there is every reason to believe that these can be overcome in the years ahead. “As percentage of the current market size, India’s latent demand is estimated at 120-150% while for China it is estimated at only 10-15%,†the report notes.

Describing the Indian luxury consumer as young (30-45 years old), it analyses that the mindset is still that of an “aspirer†not that of a “connoisseurâ€. Thus, though they value High Quality, Exclusivity and Social Appeal as key drivers of luxury purchase, they are also very Price Conscious and often straddled with a “middle-class mindsetâ€. %%

Who comprises this segment? The report suggests that medium size enterprise owners are the largest component, though the traditionally wealthy families, large industrialists and senior corporate executives are other important constituents and many self-employed professionals, young professionals, expatriates, politicians and bureaucrats also figure in the list. %%

Presently, the study notes, there is a concentration of these consumers in the ‘mainstay markets’ of Mumbai and Delhi, but projects that “in the next 5-7 years, at least 5-7 new towns will get added on the luxury map of Indiaâ€. %%

|*The report identifies four key challenges viz.*| %%

{[{{Difficulty in reaching the target consumer }}-- due to the scattered nature of the target population, absence of critical mass, and high cost of reaching them, so that word of mouth continues to be best method to create a “buzzâ€;]}

{[{{Consumer reservations about luxury purchases}} -- Most rupee millionaires have the capacity but not the propensity to spend on luxury goods and services and there are reservations against buying lesser known brands as well as shopping in India.]}

{[{{Infrastructure and regulatory constraints}} -- Lack of credible real estate options, underdeveloped back end infrastructure like warehouses and logistics as well as regulatory restrictions on FDI and high import duties.]}

{[{{Lack of talent:}} Absence of skilled manpower to provide the same customer service experience as that in international locations.}}

In conclusion it states that “The Indian consumer is in a state of flux – evolving rapidly, but perhaps along a path that is inherently different from that taken by other developing economies. While we believe there is a clear opportunity to make an impact in this market, a systematic, smart and careful approach is what will differentiate the winners from the losers in the long run.†%%

{{Jewellery as Luxury}}$$

The CII-AT Kearney study estimates the luxury products market at $1.5 billion –with Jewellery, Apparel/Accessories being the largest categories in 2009. Of these, it asserts that jewellery is the largest segment (USD 730 million growing at 25%+) and is the only product whose demand is distributed uniformly across the country.

Perhaps one of the reasons for this is that investment remains an important driver of jewellery purchases (weddings and festive buying account for a large chunk as well), and the demand for jewellery has withstood the pressures of the recession far better than other luxury products. %%

Besides the growth of the diamond jewellery category has also been significant, and luxury jewellery is estimated to account for almost 15% of this segment. %%

Analysing the luxury segment of the market, the study says, “The really top end of the market would be large high quality solitaires ( 3 carat+) and high end diamond studded jewellery (> 10 lakhs per piece). Most of these would be sold by leading family jewellers and independent jewellery designers, estimated to be around 125-150 in the whole country. International jewellery brands like Cartier, Chopard, Tiffany have been in the country for some time, although their impact on the market has been limited.†%%

A recent newspaper report claims that the demand for high end jewellery of above Rs.5 lakhs (Rs. 500,000) is growing at 50% - much above the 20% overall growth rate for the jewellery sector. %%

Says Neelesh Hundekari, principal, A T Kearney, “Designers have begun to get attention and collections based on themes are becoming well accepted. The top family jewellers focus on this segment a lot more and they have a competitive advantage due to long standing relationships with wealthy families. Many fashion designers have turned their attention to this space which complements apparel. Interviews reveal there is an almost insatiable demand for high end jewellery in the country. Unlike other luxury products, this market is more widely distributed with cities like Kolkata and Chennai having a high demand.†%%

This shift however is seen only in parts of the organised sector – the vast majority of jewellers continue to operate in the unorganised sector. %%

Says Hundekari, “Organized retail penetration has been increasing rapidly over the past few years, yet it is still very low. However, the bridal segment is still predominantly unbranded and catered to by unorganised sector (traditional / family jewellers). †%%

In addition to the large number of players in this unorganised sector, even in the modern sector there are many who persist with older traditional practices. %%

Perhaps the one that has attracted the most discussion is that of pricing – despite the high cost of the pieces, even many luxury jewellers continue to sell their products based on the time honoured ‘price of component raw materials + making charges formula’. %%

There are exceptions, but these are still individual exceptions rather than a widely followed practice. Mehul Choksi, CMD, Gitanjali Group, the pioneer of jewellery branding in India believes in the MRP model of pricing for all the diamond brands manufactured and / or marketed by his company. “Consumers are willing to pay higher prices if they believe that they are getting value for money,†he says, citing the example of the various diamond brands that his company retails in India.

“Last year, which was one of the worst that the industry has seen, we were able to raise the prices of our products on a number of occasions to keep pace with rising costs, and never did we face any consumer resistance in terms of demand,†he adds. %%

“I think that we can realise far higher prices for our products than we are getting at present, » Choksi avers, saying that the key lies in « creating aspirational demand, and promoting diamonds as an object of desire.†%%

The Group has been building iconic brands with an emotional appeal using Bollywood stars and cricketing legends in its brand promotions as they establish a connect with the consumers very easily. “There is no limit to what we can achieve and the prices we can realise as long as we have an excellent product, proper branding and well executed marketing, » a confident Choksi concludes. %%

It is an opinion seconded by Hemant Shah of Hammer Plus, who says, “If we can change the perception regarding jewellery, especially diamond jewellery, and all people wearing diamonds get a ‘flaunt’ value, jewellers can certainly expect to earn better margins. People will be willing to pay more only if they get something in return.†%%

Some months ago a panel discussion on “Emergence of Designer Jewellery and future prospects of this category†saw a lively discussion on this very theme. All the panelists including jewellery designers Varuna D. Jani, Farah Khan, Bina Goenka, Siddharth Sawansukha and Mira Gulati as well as moderator Harshad Ajoomal were unanimous that it was time for the retailers to rethink their pricing strategy particularly in regard to high end designer jewellery. %%

There is no other product where price is calculated on, and which is bought and sold on, the basis of cost of raw material plus cost of labour (making charges). From a simple pen to a car or a high fashion outfit, no one goes to a store and asks for the price of steel or silk or ink. Why then is this supposedly luxury product subject to this pricing structure? %%

The panelists passionately argued that there is a need to create a new mindset amongst both jewellers and consumers in this regard. But they put the onus of responsibility on the jewellers themselves. “If we don’t believe in our product ourselves, and defend it, how can we convince the consumer and change their attitude?†said speaker after speaker with great passion. %%

Farah Khan was quite emphatic that the industry must be clear that it is selling a dream. “We are giving an experience to the consumer when we sell unique pieces of creative designer jewelleryâ€. %%

It is indeed a watershed time for the industry – the opportunities are great, and if they are grabbed on time and in the proper manner, then the future is bright. Else, if there is an opposition to change, the moment will pass, and the industry may end up having to pay a heavy price for its reluctance to move with the times.

{{CII - AT Kearney Report: Size of the Luxury Market }}%%

CII - AT Kearney Report is based on estimates prepared after extensive compilation from different sources including interviews with key players, and a detailed analysis of the figures. %%

It places the size of the Indian luxury industry (including all luxury products, luxury services and luxury assets sold in India) in 2009 at USD 4.76 billion (at retail

prices). %%

While it notes that the total luxury market has grown at a CAGR of 13% between 2007-09, luxury products have grown at 22%, services degrew at 5% and assets grew at 18%.%%

{{Luxury products }}$$

|*Comprising:*| Most visible fashion luxury segments such as apparel, accessories, personal care, watches and jewellery as well wines, spirits and high-end electronics. $$

|*Estimated Size:*| US$ 1.5 billion$$

|*Growth:*| 15%$$

|*Key performers:*| Electronics, Wines and Spirits, Apparel and Jewellery%%

{{Luxury services }}$$

|*Estimated Size:*| US$ 0.77 billion$$

|*Growth: *|-5%$$

|*Key indicators:*| Severely hit by the recession over the past 2 years.$$

Considered to be one of the best in the world. Consumers prefer Indian hotel chains even when International chains have entered the country. %%

{{Luxury assets }}$$

|*Estimated Size:*| US$ 2.45 billion$$

|*Growth:*| 18%$$

|*Key performers:*| Real Estate and Automobiles

{{World Wealth Report: Some Highlights }}%%

{[The world’s population of high net worth individuals (HNWIs) grew 17.1% to 10.0 million in 2009.]}

{[HNWI financial wealth increased 18.9% from 2008 levels to $39 trillion. After losing 24.0% in 2008, Ultra-HNWIs saw wealth rebound 21.5% in 2009.Ultra-HNWIs increased their wealth by 21.5% in 2009.]}

{[In terms of the total Global HNWI population remains highly concentrated with the U.S, Japan and Germany accounting for 53.5% of the world’s HNWI population, down slightly from 2008.]}

{[The Asia-Pacific region was home to eight of the world’s ten fastest-growing HNWI populations, led by Hong Kong (104.4%) and India (50.9%).]}

{[In India, real GDP growth increased to 6.8% in 2009 from 6.1% in 2008.]}

{[Market capitalization in India and China almost doubled]}

{{“We must create a flaunt value for diamond jewellery to realise better marginsâ€}}%%

|*Hemant Shah, Hammer Plus*|%%

In India we have so far tended to sell jewellery as an investment. We need to move away from that approach and market the product as something that is beautiful and has an emotional appeal. %%

The price which we realise must be based on the consumer perceiving it as a luxury product. %%

There are various steps we need to take to make this a reality, but none so important as a new approach to the way we understand and present ourselves and our creations. %%

For a start we must carry out widespread promotions and education about our product so that people understand how rare and valuable diamonds really are. %%

Over and above that we must work towards a situation where every piece of jewellery is easily identifiable as a brand. Of course, this is not so easy unless every jeweller develops a signature look. Presently, it is far easier for others to identify the brand that a person is wearing in the case of a watch, rather than in the case of jewellery. %%

One way of getting around this is to step up our generic promotions. By this I mean, not just emotional appeals to the consumer, but a campaign to create a specific ‘brand’ image for ALL diamond jewellery – so that anyone wearing diamonds is immediately granted recognition as a luxury consumer. %%

If we can do this successfully and all people wearing diamonds get the value of ‘flaunt’ then we can certainly expect to earn better margins. Consumers will be willing to pay more, only if they feel they are getting something additional in return. %%

We also have another USP – diamond jewellery is not only a fantastic product, it is also the only luxury product that appreciates in value over a period of time. Of course, we must be careful how we present this – it must be seen as an additional advantage, a by-product, rather than the sole or even primary USP. %%

Retailing is the second most important area that needs attention. We must convert all aspects of the buying experience into a luxury experience. We must train our sales staff and also enhance the quality of the personnel who man the shop floor. Presently with the low margins that we earn, we are unable to employ highly skilled and qualified sales personnel. This impacts the level of service we are able to provide -- as a result the consumer experience falls well short of truly luxury standards. %%

Additionally we have to improve the design and quality of the product. A piece of diamond jewellery must be perceived as something special; the consumer must be able to feel ‘I am proud to own it’. %%

Unfortunately globally we have tended to commoditise diamonds – today everyone wears them. Without impacting the breadth of the market, we must create a different image for diamonds – and this requires a serious and thoughtful process so that we can come up with innovative ideas to promote this message. %%

Finally we must realise that every successful product category in the world today is one that is able to innovate and come out with new advancements. This is something the jewellery industry really lacks – we don’t know how to innovate. %%

We have to start thinking innovatively and realise that we are selling something that is beyond the gold and diamonds that constitute the product. We must create products that stand out, are noticed and remembered. For this we need to begin spending on R & D. Manufacturers have to take a lead and invest first in creating different types of jewellery products and other studded items, products that are easily differentiated from the others in the market. And then we have to all come together and educate the consumer about this – that will make a big difference.

{{“The external environment is positive, much can be achieved with a new mindset.â€}} %%

|*Neeelesh Hundekari, Principal, A T Kearney*|%%

Jewellers are clearly a part of the luxury segment, especially the large family jewellers who have many years of tradition behind them. Currently in India there are no international brands in this space. Moreover Indians have an inherent fascination for jewellery, and this is true all across the country. So there is a definite demand for the product. %%

Diamond jewellery will be the key product in catering to the luxury segment – Indian has and always will be a gold dominated country, so relatively it is diamonds that have developed more of an image of a luxury product. %%

But there is a lot of work to be done to achieve success in this field. A few successful examples indicate that higher price points are becoming achievable as the industry modernises and undertakes promotions. %%

How do jewellers take this process ahead and tap the potential of the luxury segment? %%

1. The industry must bring out and enhance the value proposition of the product – jewellery must be design and collection based, it must tell a story, be based on a theme so that it acquires an aura of exclusiveness. This is the most important criteria – to create the “I have what no one else has†image of exclusivity. Some attempt to achieve this has begun – jewellers have introduced branded collections and unique designs as well as some co-branded products with fashion designers. %%

2. Design is clearly coming to the fore in a few cases. Among the more forward looking jewellers, there is a willingness to invest in design and designers. Earlier there was a fear that if I publicise my designs someone else will copy them. But this is changing and today there is a willingness to project and highlight the design element as something unique. Such jewellers are now making the quality of the design and the finishing the differentiating factor and are not so worried about copying. This trend needs to be strengthened. %%

3. Finish is also getting to be extremely important as a factor in the luxury segment – Indian finish is good and there is a need to keep the standards of our product quality and finish extremely high to attain the status of a luxury product. %%

4. Quality of service is also vital. The industry needs to pamper the consumer, make him / her feel special. Retailers need to give them exclusive experiences – a lounge for, making their selection, special individual offers for special occasions, even taking jewellery to the homes of the very high end consumer. %%

5. Ambience is another essential. Stores must be redesigned as truly high end luxury stores. The display literally has to be like an exclusive museum – with an individual place for each piece and collection, specially positioned, and presented with appropriate lighting, special props, etc. The high end jeweller must make a clean break with the average store presentation -- where jewellery is literally sold like saag bhaji. %%

6. Packaging and presentation – the product must be presented as an exquisite piece that will give it an additional allure and appeal. %%

7. Promotions must be planned well and executed professionally. Jewellers must create excitement about the product, a mood in which the consumer is willing to pay a better price for it.

Investments in all these areas will surely pay off in the long run in terms of price. Experience is showing that people are more than willing to pay a higher price for the product if it has the correct positioning and appeal. %%

There are many different niches that can be created for such an effect – the Jodha Akbar line of jewellery, for example, was an excellent idea. Other niche collections can also be developed – for example each of the 25 odd Indian states has its own traditional designs, these can inspire modern collections, perhaps even a cross pollination across states to create something new and exciting? Similarly, one can create a niche by selling say Italian jewellery in an exclusive salon environment. %%

It is most important to realise that moving in this direction is feasible because it only requires an internal change and it is in the jewellers own hands to take the step. The external environment is positive and much can be achieved if industry players develop a new mindset.

{{Critical success factors for success }}%%

Grow your footprint$$

{[Expand beyond your comfort zone: New towns, formats}]

{[Micro-segmentation: Based on occupation, community, location, life status}]

{[Personalised outreach: Develop focused modes of communication}]

{[Innovative media choices: To reach the non consumers}]

{[Break the myth: About the prices being high in India}]

Create a brand

{[Store is your brand, invest in store look and feel}]

{[Emphasise and get a value for design}]

{[Provide an experience: A reason beyond shopping}]

Get your cost structure/funding right

{[New formats: Multi-brand formats, luxury discounters, airport stores }]

{[Marketing/People Costs: Spend more}]

{[Real estate skills: Develop local skills for dealing with this non-transparent and complex market}]

{[Transparency to leverage funding options}]

Create the business environment

{[Eco-system: Education, Supply chain, Media}]

Excerpted from Presentation on |*“Luxury & Jewellery Markets in Indiaâ€*| by Neelesh Hundekari at International Diamond Conference – Mines to Markets, Mumbai Oct 13, 2010

Over the last decade, as the earnings and wealth of Indian consumers have soared, attitudes towards luxury have begun to change and the demand for high value goods and services has begun to shoot up significantly. Young Indians do not frown over conspicuous consumption unlike their forefathers; riches are being acquired without embarrassment and luxury labels are being flaunted with confidence and pride.%%

Recent studies indicate that this is only the tip of the iceberg, and the demand for luxury goods and services is poised to explode in terms of both volume and geographical spread over the next few years. %%

While this is clearly exciting news for jewellers in India, it also brings to the forefront a contradiction that they have always faced – jewellery is the only high value product that is actually priced and sold like a commodity rather than a luxury item. %%

The ‘cost of materials plus making charges formula’ that is predominant throughout the country squeezes margins, and impacts branding, marketing, sales and service and all the other related activities that are necessary for jewellery to be perceived and purchased as a luxury item. %%

Stephen Rego analyses some aspects of the Indian luxury market and the emerging luxury consumer, and discusses some pertinent questions about what jewellers need to do to tap the enormous potential in this sphere. %%

The last few months have brought good news for the Indian jewellery industry -- in the form of three major studies related to the luxury market. %%

The first was the Luxury Goods Worldwide Market Study, by global business and strategy consulting firm Bain & Company, which reported that the global luxury market, severely impacted during the last two years by the financial crisis was now showing signs of recovery. %%

The report predicted a 10% rise in sales in this sector to € 168 bn this year and noted that this would continue into 2011, by when the global luxury-goods sector is expected to return to pre-crisis levels. In April this year, Bain had projected a 4% growth rate, but revised this upward by October due to stronger-than-expected economic growth. %%

Part of this growth would be boosted by favourable exchange rates, but the role of shoppers from the two booming Asian economies – India and China – would also be significant. Interestingly Bain & Co’s report saw the impact of these two countries is taking place at two levels – strong growth of domestic demand for luxury goods in both countries and the “increasing flows of Asian and Chinese shoppers to Europeâ€.

According to the U.S. consultancy the overall rise in demand in the luxury sector could be attributed to an increase in international travel, a boom in e-commerce and a good performance of the retail sector. Bain & Co also forecast that though the pace of growth should slow to between 3% and 5% to € 173 to 176 billion, it would have crossed the pre-crisis peak of € 170 billion registered in 2007 by then. %%

On a global scale, Bain identified the emerging Asian markets, particularly China, which at present is the fastest-growing luxury market, as being the drivers of this surge. While this may sound positive for the Indian luxury industry, a closer look reveals that the picture is not so rosy. %%

Though in terms of absolute numbers, India with its billion plus population is almost as big a market as China, in the luxury sector it lags far behind. The report estimates the size of the luxury market at € 800 million, and projects a healthy 4-5% growth during the year. %%

But these figures are not so impressive when compared to our Asian neighbour, China, with a market size of € 9.2 billion and massive 30% year-on-year growth in 2008, 20% in 2009, and a predicted 30% in 2010. %%

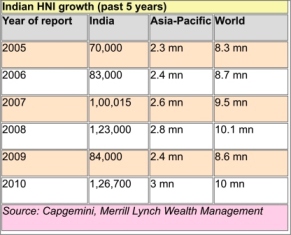

Another recently released document, The World Wealth Report 2010 by Capgemini and Merrill Lynch, however analyses the potential of the Indian luxury market from a slightly different perspective – that of the numbers of HNIs (High Net Worth Individuals). %%

It has some startling facts that confirm what many analysts have been suggesting – that Asia Pacific is the growth engine of the coming decade. The report notes that at 3 million the numbers of HNIs in the Asia-Pacific region now equals that of Europe and that the wealth generated by individuals there is now larger than that of Europe. The total wealth of this segment in the Asia Pacific now stands at $9.7 trillion (up 30.9% over the previous year), inching ahead of the $9.5 trillion held by Europe's HNIs. %%

The surge is particularly marked in India — where the population of HNIs (having minimum investible assets of USD 1mn) surged 50.9% to 1,26,700 in 2009 from 84,000 the previous year. This was significantly faster than the 20.4% and 30.4% growth in the number of HNIs in the world and Asia-Pacific region respectively, and represents a huge 81% increase when compared to the absolute numbers in 2005.

Releasing the report, Pradeep Dokania, chairman, Merrill Lynch global wealth management, India, noted, "The rebound in HNI numbers is highly correlated to the strong recovery in stock prices and strong outlook for India's underlying economy." %%

Significantly, wealth generation in India is seen both at the very high end and the upper middle class segments and is expected to continue to register strong growth in the coming years. %%

Other reports not directly related to the luxury segment confirm this assessment. For example, according to NCAER (2009) survey - India has 46.7 million high income households1 as compared to 41 million in the low income category. Middle income households surged to 140.7 million (300 m adults) out of the total of 228.4 Indian million families at the end of 2009-10. (Average 5 persons per household – 2 adults). %%

THIS IS A FOOTNOTE( Households earning less than Rs. 40,000 per annum (at 2001-02 prices) are dubbed as low income, whereas those with earnings over Rs. 1.80 lakh fall in the high income category. Those earning between Rs. 45,000-Rs 1.80 lakh per annum are considered middle income households.) %%

Further, a study by the McKinsey Global Institute titled The Bird of Gold: The Rise of India’s Consumer Market suggests that if India continues its growth, the average household disposable incomes will more than double in the next 15 years from Rs.1,20,000 in 2010 to Rs.3,00,000 in 2025. %%

Returning to the luxury market, the third recently released report referred to earlier was a study entitled Luxury in India: Charming the Snakes and Scaling the Ladders prepared and published by Confederation of Indian Industry (CII) and A T Kearney. The report was released at the second edition of the CII’s Luxury Goods Forum held in Delhi on October 7, 2010 as part of the Commonwealth Games Business Forum. %%

The report estimates that in 2009 India's luxury industry including products, services and assets stood at $4.76 billion. Though this is small compared to global standards, the figure is expected to grow three times and touch $14.7 billion by 2015. %%

The study believes that there is a massive ‘latent demand’ as growth of the luxury industry has been constrained by both supply and demand side factors in the past, but there is every reason to believe that these can be overcome in the years ahead. “As percentage of the current market size, India’s latent demand is estimated at 120-150% while for China it is estimated at only 10-15%,†the report notes.

Describing the Indian luxury consumer as young (30-45 years old), it analyses that the mindset is still that of an “aspirer†not that of a “connoisseurâ€. Thus, though they value High Quality, Exclusivity and Social Appeal as key drivers of luxury purchase, they are also very Price Conscious and often straddled with a “middle-class mindsetâ€. %%

Who comprises this segment? The report suggests that medium size enterprise owners are the largest component, though the traditionally wealthy families, large industrialists and senior corporate executives are other important constituents and many self-employed professionals, young professionals, expatriates, politicians and bureaucrats also figure in the list. %%

Presently, the study notes, there is a concentration of these consumers in the ‘mainstay markets’ of Mumbai and Delhi, but projects that “in the next 5-7 years, at least 5-7 new towns will get added on the luxury map of Indiaâ€. %%

|*The report identifies four key challenges viz.*| %%

{[{{Difficulty in reaching the target consumer }}-- due to the scattered nature of the target population, absence of critical mass, and high cost of reaching them, so that word of mouth continues to be best method to create a “buzzâ€;]}

{[{{Consumer reservations about luxury purchases}} -- Most rupee millionaires have the capacity but not the propensity to spend on luxury goods and services and there are reservations against buying lesser known brands as well as shopping in India.]}

{[{{Infrastructure and regulatory constraints}} -- Lack of credible real estate options, underdeveloped back end infrastructure like warehouses and logistics as well as regulatory restrictions on FDI and high import duties.]}

{[{{Lack of talent:}} Absence of skilled manpower to provide the same customer service experience as that in international locations.}}

In conclusion it states that “The Indian consumer is in a state of flux – evolving rapidly, but perhaps along a path that is inherently different from that taken by other developing economies. While we believe there is a clear opportunity to make an impact in this market, a systematic, smart and careful approach is what will differentiate the winners from the losers in the long run.†%%

{{Jewellery as Luxury}}$$

The CII-AT Kearney study estimates the luxury products market at $1.5 billion –with Jewellery, Apparel/Accessories being the largest categories in 2009. Of these, it asserts that jewellery is the largest segment (USD 730 million growing at 25%+) and is the only product whose demand is distributed uniformly across the country.

Perhaps one of the reasons for this is that investment remains an important driver of jewellery purchases (weddings and festive buying account for a large chunk as well), and the demand for jewellery has withstood the pressures of the recession far better than other luxury products. %%

Besides the growth of the diamond jewellery category has also been significant, and luxury jewellery is estimated to account for almost 15% of this segment. %%

Analysing the luxury segment of the market, the study says, “The really top end of the market would be large high quality solitaires ( 3 carat+) and high end diamond studded jewellery (> 10 lakhs per piece). Most of these would be sold by leading family jewellers and independent jewellery designers, estimated to be around 125-150 in the whole country. International jewellery brands like Cartier, Chopard, Tiffany have been in the country for some time, although their impact on the market has been limited.†%%

A recent newspaper report claims that the demand for high end jewellery of above Rs.5 lakhs (Rs. 500,000) is growing at 50% - much above the 20% overall growth rate for the jewellery sector. %%

Says Neelesh Hundekari, principal, A T Kearney, “Designers have begun to get attention and collections based on themes are becoming well accepted. The top family jewellers focus on this segment a lot more and they have a competitive advantage due to long standing relationships with wealthy families. Many fashion designers have turned their attention to this space which complements apparel. Interviews reveal there is an almost insatiable demand for high end jewellery in the country. Unlike other luxury products, this market is more widely distributed with cities like Kolkata and Chennai having a high demand.†%%

This shift however is seen only in parts of the organised sector – the vast majority of jewellers continue to operate in the unorganised sector. %%

Says Hundekari, “Organized retail penetration has been increasing rapidly over the past few years, yet it is still very low. However, the bridal segment is still predominantly unbranded and catered to by unorganised sector (traditional / family jewellers). †%%

In addition to the large number of players in this unorganised sector, even in the modern sector there are many who persist with older traditional practices. %%

Perhaps the one that has attracted the most discussion is that of pricing – despite the high cost of the pieces, even many luxury jewellers continue to sell their products based on the time honoured ‘price of component raw materials + making charges formula’. %%

There are exceptions, but these are still individual exceptions rather than a widely followed practice. Mehul Choksi, CMD, Gitanjali Group, the pioneer of jewellery branding in India believes in the MRP model of pricing for all the diamond brands manufactured and / or marketed by his company. “Consumers are willing to pay higher prices if they believe that they are getting value for money,†he says, citing the example of the various diamond brands that his company retails in India.

“Last year, which was one of the worst that the industry has seen, we were able to raise the prices of our products on a number of occasions to keep pace with rising costs, and never did we face any consumer resistance in terms of demand,†he adds. %%

“I think that we can realise far higher prices for our products than we are getting at present, » Choksi avers, saying that the key lies in « creating aspirational demand, and promoting diamonds as an object of desire.†%%

The Group has been building iconic brands with an emotional appeal using Bollywood stars and cricketing legends in its brand promotions as they establish a connect with the consumers very easily. “There is no limit to what we can achieve and the prices we can realise as long as we have an excellent product, proper branding and well executed marketing, » a confident Choksi concludes. %%

It is an opinion seconded by Hemant Shah of Hammer Plus, who says, “If we can change the perception regarding jewellery, especially diamond jewellery, and all people wearing diamonds get a ‘flaunt’ value, jewellers can certainly expect to earn better margins. People will be willing to pay more only if they get something in return.†%%

Some months ago a panel discussion on “Emergence of Designer Jewellery and future prospects of this category†saw a lively discussion on this very theme. All the panelists including jewellery designers Varuna D. Jani, Farah Khan, Bina Goenka, Siddharth Sawansukha and Mira Gulati as well as moderator Harshad Ajoomal were unanimous that it was time for the retailers to rethink their pricing strategy particularly in regard to high end designer jewellery. %%

There is no other product where price is calculated on, and which is bought and sold on, the basis of cost of raw material plus cost of labour (making charges). From a simple pen to a car or a high fashion outfit, no one goes to a store and asks for the price of steel or silk or ink. Why then is this supposedly luxury product subject to this pricing structure? %%

The panelists passionately argued that there is a need to create a new mindset amongst both jewellers and consumers in this regard. But they put the onus of responsibility on the jewellers themselves. “If we don’t believe in our product ourselves, and defend it, how can we convince the consumer and change their attitude?†said speaker after speaker with great passion. %%

Farah Khan was quite emphatic that the industry must be clear that it is selling a dream. “We are giving an experience to the consumer when we sell unique pieces of creative designer jewelleryâ€. %%

It is indeed a watershed time for the industry – the opportunities are great, and if they are grabbed on time and in the proper manner, then the future is bright. Else, if there is an opposition to change, the moment will pass, and the industry may end up having to pay a heavy price for its reluctance to move with the times.

{{CII - AT Kearney Report: Size of the Luxury Market }}%%

CII - AT Kearney Report is based on estimates prepared after extensive compilation from different sources including interviews with key players, and a detailed analysis of the figures. %%

It places the size of the Indian luxury industry (including all luxury products, luxury services and luxury assets sold in India) in 2009 at USD 4.76 billion (at retail

prices). %%

While it notes that the total luxury market has grown at a CAGR of 13% between 2007-09, luxury products have grown at 22%, services degrew at 5% and assets grew at 18%.%%

{{Luxury products }}$$

|*Comprising:*| Most visible fashion luxury segments such as apparel, accessories, personal care, watches and jewellery as well wines, spirits and high-end electronics. $$

|*Estimated Size:*| US$ 1.5 billion$$

|*Growth:*| 15%$$

|*Key performers:*| Electronics, Wines and Spirits, Apparel and Jewellery%%

{{Luxury services }}$$

|*Estimated Size:*| US$ 0.77 billion$$

|*Growth: *|-5%$$

|*Key indicators:*| Severely hit by the recession over the past 2 years.$$

Considered to be one of the best in the world. Consumers prefer Indian hotel chains even when International chains have entered the country. %%

{{Luxury assets }}$$

|*Estimated Size:*| US$ 2.45 billion$$

|*Growth:*| 18%$$

|*Key performers:*| Real Estate and Automobiles

{{World Wealth Report: Some Highlights }}%%

{[The world’s population of high net worth individuals (HNWIs) grew 17.1% to 10.0 million in 2009.]}

{[HNWI financial wealth increased 18.9% from 2008 levels to $39 trillion. After losing 24.0% in 2008, Ultra-HNWIs saw wealth rebound 21.5% in 2009.Ultra-HNWIs increased their wealth by 21.5% in 2009.]}

{[In terms of the total Global HNWI population remains highly concentrated with the U.S, Japan and Germany accounting for 53.5% of the world’s HNWI population, down slightly from 2008.]}

{[The Asia-Pacific region was home to eight of the world’s ten fastest-growing HNWI populations, led by Hong Kong (104.4%) and India (50.9%).]}

{[In India, real GDP growth increased to 6.8% in 2009 from 6.1% in 2008.]}

{[Market capitalization in India and China almost doubled]}

{{“We must create a flaunt value for diamond jewellery to realise better marginsâ€}}%%

|*Hemant Shah, Hammer Plus*|%%

In India we have so far tended to sell jewellery as an investment. We need to move away from that approach and market the product as something that is beautiful and has an emotional appeal. %%

The price which we realise must be based on the consumer perceiving it as a luxury product. %%

There are various steps we need to take to make this a reality, but none so important as a new approach to the way we understand and present ourselves and our creations. %%

For a start we must carry out widespread promotions and education about our product so that people understand how rare and valuable diamonds really are. %%

Over and above that we must work towards a situation where every piece of jewellery is easily identifiable as a brand. Of course, this is not so easy unless every jeweller develops a signature look. Presently, it is far easier for others to identify the brand that a person is wearing in the case of a watch, rather than in the case of jewellery. %%

One way of getting around this is to step up our generic promotions. By this I mean, not just emotional appeals to the consumer, but a campaign to create a specific ‘brand’ image for ALL diamond jewellery – so that anyone wearing diamonds is immediately granted recognition as a luxury consumer. %%

If we can do this successfully and all people wearing diamonds get the value of ‘flaunt’ then we can certainly expect to earn better margins. Consumers will be willing to pay more, only if they feel they are getting something additional in return. %%

We also have another USP – diamond jewellery is not only a fantastic product, it is also the only luxury product that appreciates in value over a period of time. Of course, we must be careful how we present this – it must be seen as an additional advantage, a by-product, rather than the sole or even primary USP. %%

Retailing is the second most important area that needs attention. We must convert all aspects of the buying experience into a luxury experience. We must train our sales staff and also enhance the quality of the personnel who man the shop floor. Presently with the low margins that we earn, we are unable to employ highly skilled and qualified sales personnel. This impacts the level of service we are able to provide -- as a result the consumer experience falls well short of truly luxury standards. %%

Additionally we have to improve the design and quality of the product. A piece of diamond jewellery must be perceived as something special; the consumer must be able to feel ‘I am proud to own it’. %%

Unfortunately globally we have tended to commoditise diamonds – today everyone wears them. Without impacting the breadth of the market, we must create a different image for diamonds – and this requires a serious and thoughtful process so that we can come up with innovative ideas to promote this message. %%

Finally we must realise that every successful product category in the world today is one that is able to innovate and come out with new advancements. This is something the jewellery industry really lacks – we don’t know how to innovate. %%

We have to start thinking innovatively and realise that we are selling something that is beyond the gold and diamonds that constitute the product. We must create products that stand out, are noticed and remembered. For this we need to begin spending on R & D. Manufacturers have to take a lead and invest first in creating different types of jewellery products and other studded items, products that are easily differentiated from the others in the market. And then we have to all come together and educate the consumer about this – that will make a big difference.

{{“The external environment is positive, much can be achieved with a new mindset.â€}} %%

|*Neeelesh Hundekari, Principal, A T Kearney*|%%

Jewellers are clearly a part of the luxury segment, especially the large family jewellers who have many years of tradition behind them. Currently in India there are no international brands in this space. Moreover Indians have an inherent fascination for jewellery, and this is true all across the country. So there is a definite demand for the product. %%

Diamond jewellery will be the key product in catering to the luxury segment – Indian has and always will be a gold dominated country, so relatively it is diamonds that have developed more of an image of a luxury product. %%

But there is a lot of work to be done to achieve success in this field. A few successful examples indicate that higher price points are becoming achievable as the industry modernises and undertakes promotions. %%

How do jewellers take this process ahead and tap the potential of the luxury segment? %%

1. The industry must bring out and enhance the value proposition of the product – jewellery must be design and collection based, it must tell a story, be based on a theme so that it acquires an aura of exclusiveness. This is the most important criteria – to create the “I have what no one else has†image of exclusivity. Some attempt to achieve this has begun – jewellers have introduced branded collections and unique designs as well as some co-branded products with fashion designers. %%

2. Design is clearly coming to the fore in a few cases. Among the more forward looking jewellers, there is a willingness to invest in design and designers. Earlier there was a fear that if I publicise my designs someone else will copy them. But this is changing and today there is a willingness to project and highlight the design element as something unique. Such jewellers are now making the quality of the design and the finishing the differentiating factor and are not so worried about copying. This trend needs to be strengthened. %%

3. Finish is also getting to be extremely important as a factor in the luxury segment – Indian finish is good and there is a need to keep the standards of our product quality and finish extremely high to attain the status of a luxury product. %%

4. Quality of service is also vital. The industry needs to pamper the consumer, make him / her feel special. Retailers need to give them exclusive experiences – a lounge for, making their selection, special individual offers for special occasions, even taking jewellery to the homes of the very high end consumer. %%

5. Ambience is another essential. Stores must be redesigned as truly high end luxury stores. The display literally has to be like an exclusive museum – with an individual place for each piece and collection, specially positioned, and presented with appropriate lighting, special props, etc. The high end jeweller must make a clean break with the average store presentation -- where jewellery is literally sold like saag bhaji. %%

6. Packaging and presentation – the product must be presented as an exquisite piece that will give it an additional allure and appeal. %%

7. Promotions must be planned well and executed professionally. Jewellers must create excitement about the product, a mood in which the consumer is willing to pay a better price for it.

Investments in all these areas will surely pay off in the long run in terms of price. Experience is showing that people are more than willing to pay a higher price for the product if it has the correct positioning and appeal. %%

There are many different niches that can be created for such an effect – the Jodha Akbar line of jewellery, for example, was an excellent idea. Other niche collections can also be developed – for example each of the 25 odd Indian states has its own traditional designs, these can inspire modern collections, perhaps even a cross pollination across states to create something new and exciting? Similarly, one can create a niche by selling say Italian jewellery in an exclusive salon environment. %%

It is most important to realise that moving in this direction is feasible because it only requires an internal change and it is in the jewellers own hands to take the step. The external environment is positive and much can be achieved if industry players develop a new mindset.

{{Critical success factors for success }}%%

Grow your footprint$$

{[Expand beyond your comfort zone: New towns, formats}]

{[Micro-segmentation: Based on occupation, community, location, life status}]

{[Personalised outreach: Develop focused modes of communication}]

{[Innovative media choices: To reach the non consumers}]

{[Break the myth: About the prices being high in India}]

Create a brand

{[Store is your brand, invest in store look and feel}]

{[Emphasise and get a value for design}]

{[Provide an experience: A reason beyond shopping}]

Get your cost structure/funding right

{[New formats: Multi-brand formats, luxury discounters, airport stores }]

{[Marketing/People Costs: Spend more}]

{[Real estate skills: Develop local skills for dealing with this non-transparent and complex market}]

{[Transparency to leverage funding options}]

Create the business environment

{[Eco-system: Education, Supply chain, Media}]

Excerpted from Presentation on |*“Luxury & Jewellery Markets in Indiaâ€*| by Neelesh Hundekari at International Diamond Conference – Mines to Markets, Mumbai Oct 13, 2010

Over the last decade, as the earnings and wealth of Indian consumers have soared, attitudes towards luxury have begun to change and the demand for high value goods and services has begun to shoot up significantly. Young Indians do not frown over conspicuous consumption unlike their forefathers; riches are being acquired without embarrassment and luxury labels are being flaunted with confidence and pride.%%

Recent studies indicate that this is only the tip of the iceberg, and the demand for luxury goods and services is poised to explode in terms of both volume and geographical spread over the next few years. %%

While this is clearly exciting news for jewellers in India, it also brings to the forefront a contradiction that they have always faced – jewellery is the only high value product that is actually priced and sold like a commodity rather than a luxury item. %%

The ‘cost of materials plus making charges formula’ that is predominant throughout the country squeezes margins, and impacts branding, marketing, sales and service and all the other related activities that are necessary for jewellery to be perceived and purchased as a luxury item. %%

Stephen Rego analyses some aspects of the Indian luxury market and the emerging luxury consumer, and discusses some pertinent questions about what jewellers need to do to tap the enormous potential in this sphere. %%

The last few months have brought good news for the Indian jewellery industry -- in the form of three major studies related to the luxury market. %%

The first was the Luxury Goods Worldwide Market Study, by global business and strategy consulting firm Bain & Company, which reported that the global luxury market, severely impacted during the last two years by the financial crisis was now showing signs of recovery. %%

The report predicted a 10% rise in sales in this sector to € 168 bn this year and noted that this would continue into 2011, by when the global luxury-goods sector is expected to return to pre-crisis levels. In April this year, Bain had projected a 4% growth rate, but revised this upward by October due to stronger-than-expected economic growth. %%

Part of this growth would be boosted by favourable exchange rates, but the role of shoppers from the two booming Asian economies – India and China – would also be significant. Interestingly Bain & Co’s report saw the impact of these two countries is taking place at two levels – strong growth of domestic demand for luxury goods in both countries and the “increasing flows of Asian and Chinese shoppers to Europeâ€.

According to the U.S. consultancy the overall rise in demand in the luxury sector could be attributed to an increase in international travel, a boom in e-commerce and a good performance of the retail sector. Bain & Co also forecast that though the pace of growth should slow to between 3% and 5% to € 173 to 176 billion, it would have crossed the pre-crisis peak of € 170 billion registered in 2007 by then. %%

On a global scale, Bain identified the emerging Asian markets, particularly China, which at present is the fastest-growing luxury market, as being the drivers of this surge. While this may sound positive for the Indian luxury industry, a closer look reveals that the picture is not so rosy. %%

Though in terms of absolute numbers, India with its billion plus population is almost as big a market as China, in the luxury sector it lags far behind. The report estimates the size of the luxury market at € 800 million, and projects a healthy 4-5% growth during the year. %%

But these figures are not so impressive when compared to our Asian neighbour, China, with a market size of € 9.2 billion and massive 30% year-on-year growth in 2008, 20% in 2009, and a predicted 30% in 2010. %%

Another recently released document, The World Wealth Report 2010 by Capgemini and Merrill Lynch, however analyses the potential of the Indian luxury market from a slightly different perspective – that of the numbers of HNIs (High Net Worth Individuals). %%

It has some startling facts that confirm what many analysts have been suggesting – that Asia Pacific is the growth engine of the coming decade. The report notes that at 3 million the numbers of HNIs in the Asia-Pacific region now equals that of Europe and that the wealth generated by individuals there is now larger than that of Europe. The total wealth of this segment in the Asia Pacific now stands at $9.7 trillion (up 30.9% over the previous year), inching ahead of the $9.5 trillion held by Europe's HNIs. %%

The surge is particularly marked in India — where the population of HNIs (having minimum investible assets of USD 1mn) surged 50.9% to 1,26,700 in 2009 from 84,000 the previous year. This was significantly faster than the 20.4% and 30.4% growth in the number of HNIs in the world and Asia-Pacific region respectively, and represents a huge 81% increase when compared to the absolute numbers in 2005.

Releasing the report, Pradeep Dokania, chairman, Merrill Lynch global wealth management, India, noted, "The rebound in HNI numbers is highly correlated to the strong recovery in stock prices and strong outlook for India's underlying economy." %%

Significantly, wealth generation in India is seen both at the very high end and the upper middle class segments and is expected to continue to register strong growth in the coming years. %%

Other reports not directly related to the luxury segment confirm this assessment. For example, according to NCAER (2009) survey - India has 46.7 million high income households1 as compared to 41 million in the low income category. Middle income households surged to 140.7 million (300 m adults) out of the total of 228.4 Indian million families at the end of 2009-10. (Average 5 persons per household – 2 adults). %%

THIS IS A FOOTNOTE( Households earning less than Rs. 40,000 per annum (at 2001-02 prices) are dubbed as low income, whereas those with earnings over Rs. 1.80 lakh fall in the high income category. Those earning between Rs. 45,000-Rs 1.80 lakh per annum are considered middle income households.) %%

Further, a study by the McKinsey Global Institute titled The Bird of Gold: The Rise of India’s Consumer Market suggests that if India continues its growth, the average household disposable incomes will more than double in the next 15 years from Rs.1,20,000 in 2010 to Rs.3,00,000 in 2025. %%

Returning to the luxury market, the third recently released report referred to earlier was a study entitled Luxury in India: Charming the Snakes and Scaling the Ladders prepared and published by Confederation of Indian Industry (CII) and A T Kearney. The report was released at the second edition of the CII’s Luxury Goods Forum held in Delhi on October 7, 2010 as part of the Commonwealth Games Business Forum. %%

The report estimates that in 2009 India's luxury industry including products, services and assets stood at $4.76 billion. Though this is small compared to global standards, the figure is expected to grow three times and touch $14.7 billion by 2015. %%

The study believes that there is a massive ‘latent demand’ as growth of the luxury industry has been constrained by both supply and demand side factors in the past, but there is every reason to believe that these can be overcome in the years ahead. “As percentage of the current market size, India’s latent demand is estimated at 120-150% while for China it is estimated at only 10-15%,†the report notes.

Describing the Indian luxury consumer as young (30-45 years old), it analyses that the mindset is still that of an “aspirer†not that of a “connoisseurâ€. Thus, though they value High Quality, Exclusivity and Social Appeal as key drivers of luxury purchase, they are also very Price Conscious and often straddled with a “middle-class mindsetâ€. %%

Who comprises this segment? The report suggests that medium size enterprise owners are the largest component, though the traditionally wealthy families, large industrialists and senior corporate executives are other important constituents and many self-employed professionals, young professionals, expatriates, politicians and bureaucrats also figure in the list. %%

Presently, the study notes, there is a concentration of these consumers in the ‘mainstay markets’ of Mumbai and Delhi, but projects that “in the next 5-7 years, at least 5-7 new towns will get added on the luxury map of Indiaâ€. %%

|*The report identifies four key challenges viz.*| %%

{[{{Difficulty in reaching the target consumer }}-- due to the scattered nature of the target population, absence of critical mass, and high cost of reaching them, so that word of mouth continues to be best method to create a “buzzâ€;]}

{[{{Consumer reservations about luxury purchases}} -- Most rupee millionaires have the capacity but not the propensity to spend on luxury goods and services and there are reservations against buying lesser known brands as well as shopping in India.]}

{[{{Infrastructure and regulatory constraints}} -- Lack of credible real estate options, underdeveloped back end infrastructure like warehouses and logistics as well as regulatory restrictions on FDI and high import duties.]}

{[{{Lack of talent:}} Absence of skilled manpower to provide the same customer service experience as that in international locations.}}

In conclusion it states that “The Indian consumer is in a state of flux – evolving rapidly, but perhaps along a path that is inherently different from that taken by other developing economies. While we believe there is a clear opportunity to make an impact in this market, a systematic, smart and careful approach is what will differentiate the winners from the losers in the long run.†%%

{{Jewellery as Luxury}}$$

The CII-AT Kearney study estimates the luxury products market at $1.5 billion –with Jewellery, Apparel/Accessories being the largest categories in 2009. Of these, it asserts that jewellery is the largest segment (USD 730 million growing at 25%+) and is the only product whose demand is distributed uniformly across the country.

Perhaps one of the reasons for this is that investment remains an important driver of jewellery purchases (weddings and festive buying account for a large chunk as well), and the demand for jewellery has withstood the pressures of the recession far better than other luxury products. %%

Besides the growth of the diamond jewellery category has also been significant, and luxury jewellery is estimated to account for almost 15% of this segment. %%

Analysing the luxury segment of the market, the study says, “The really top end of the market would be large high quality solitaires ( 3 carat+) and high end diamond studded jewellery (> 10 lakhs per piece). Most of these would be sold by leading family jewellers and independent jewellery designers, estimated to be around 125-150 in the whole country. International jewellery brands like Cartier, Chopard, Tiffany have been in the country for some time, although their impact on the market has been limited.†%%

A recent newspaper report claims that the demand for high end jewellery of above Rs.5 lakhs (Rs. 500,000) is growing at 50% - much above the 20% overall growth rate for the jewellery sector. %%

Says Neelesh Hundekari, principal, A T Kearney, “Designers have begun to get attention and collections based on themes are becoming well accepted. The top family jewellers focus on this segment a lot more and they have a competitive advantage due to long standing relationships with wealthy families. Many fashion designers have turned their attention to this space which complements apparel. Interviews reveal there is an almost insatiable demand for high end jewellery in the country. Unlike other luxury products, this market is more widely distributed with cities like Kolkata and Chennai having a high demand.†%%

This shift however is seen only in parts of the organised sector – the vast majority of jewellers continue to operate in the unorganised sector. %%

Says Hundekari, “Organized retail penetration has been increasing rapidly over the past few years, yet it is still very low. However, the bridal segment is still predominantly unbranded and catered to by unorganised sector (traditional / family jewellers). †%%

In addition to the large number of players in this unorganised sector, even in the modern sector there are many who persist with older traditional practices. %%

Perhaps the one that has attracted the most discussion is that of pricing – despite the high cost of the pieces, even many luxury jewellers continue to sell their products based on the time honoured ‘price of component raw materials + making charges formula’. %%

There are exceptions, but these are still individual exceptions rather than a widely followed practice. Mehul Choksi, CMD, Gitanjali Group, the pioneer of jewellery branding in India believes in the MRP model of pricing for all the diamond brands manufactured and / or marketed by his company. “Consumers are willing to pay higher prices if they believe that they are getting value for money,†he says, citing the example of the various diamond brands that his company retails in India.

“Last year, which was one of the worst that the industry has seen, we were able to raise the prices of our products on a number of occasions to keep pace with rising costs, and never did we face any consumer resistance in terms of demand,†he adds. %%

“I think that we can realise far higher prices for our products than we are getting at present, » Choksi avers, saying that the key lies in « creating aspirational demand, and promoting diamonds as an object of desire.†%%

The Group has been building iconic brands with an emotional appeal using Bollywood stars and cricketing legends in its brand promotions as they establish a connect with the consumers very easily. “There is no limit to what we can achieve and the prices we can realise as long as we have an excellent product, proper branding and well executed marketing, » a confident Choksi concludes. %%

It is an opinion seconded by Hemant Shah of Hammer Plus, who says, “If we can change the perception regarding jewellery, especially diamond jewellery, and all people wearing diamonds get a ‘flaunt’ value, jewellers can certainly expect to earn better margins. People will be willing to pay more only if they get something in return.†%%

Some months ago a panel discussion on “Emergence of Designer Jewellery and future prospects of this category†saw a lively discussion on this very theme. All the panelists including jewellery designers Varuna D. Jani, Farah Khan, Bina Goenka, Siddharth Sawansukha and Mira Gulati as well as moderator Harshad Ajoomal were unanimous that it was time for the retailers to rethink their pricing strategy particularly in regard to high end designer jewellery. %%

There is no other product where price is calculated on, and which is bought and sold on, the basis of cost of raw material plus cost of labour (making charges). From a simple pen to a car or a high fashion outfit, no one goes to a store and asks for the price of steel or silk or ink. Why then is this supposedly luxury product subject to this pricing structure? %%

The panelists passionately argued that there is a need to create a new mindset amongst both jewellers and consumers in this regard. But they put the onus of responsibility on the jewellers themselves. “If we don’t believe in our product ourselves, and defend it, how can we convince the consumer and change their attitude?†said speaker after speaker with great passion. %%

Farah Khan was quite emphatic that the industry must be clear that it is selling a dream. “We are giving an experience to the consumer when we sell unique pieces of creative designer jewelleryâ€. %%

It is indeed a watershed time for the industry – the opportunities are great, and if they are grabbed on time and in the proper manner, then the future is bright. Else, if there is an opposition to change, the moment will pass, and the industry may end up having to pay a heavy price for its reluctance to move with the times.

{{CII - AT Kearney Report: Size of the Luxury Market }}%%

CII - AT Kearney Report is based on estimates prepared after extensive compilation from different sources including interviews with key players, and a detailed analysis of the figures. %%

It places the size of the Indian luxury industry (including all luxury products, luxury services and luxury assets sold in India) in 2009 at USD 4.76 billion (at retail

prices). %%

While it notes that the total luxury market has grown at a CAGR of 13% between 2007-09, luxury products have grown at 22%, services degrew at 5% and assets grew at 18%.%%

{{Luxury products }}$$

|*Comprising:*| Most visible fashion luxury segments such as apparel, accessories, personal care, watches and jewellery as well wines, spirits and high-end electronics. $$

|*Estimated Size:*| US$ 1.5 billion$$

|*Growth:*| 15%$$

|*Key performers:*| Electronics, Wines and Spirits, Apparel and Jewellery%%

{{Luxury services }}$$

|*Estimated Size:*| US$ 0.77 billion$$

|*Growth: *|-5%$$

|*Key indicators:*| Severely hit by the recession over the past 2 years.$$

Considered to be one of the best in the world. Consumers prefer Indian hotel chains even when International chains have entered the country. %%

{{Luxury assets }}$$

|*Estimated Size:*| US$ 2.45 billion$$

|*Growth:*| 18%$$

|*Key performers:*| Real Estate and Automobiles

{{World Wealth Report: Some Highlights }}%%

{[The world’s population of high net worth individuals (HNWIs) grew 17.1% to 10.0 million in 2009.]}

{[HNWI financial wealth increased 18.9% from 2008 levels to $39 trillion. After losing 24.0% in 2008, Ultra-HNWIs saw wealth rebound 21.5% in 2009.Ultra-HNWIs increased their wealth by 21.5% in 2009.]}

{[In terms of the total Global HNWI population remains highly concentrated with the U.S, Japan and Germany accounting for 53.5% of the world’s HNWI population, down slightly from 2008.]}

{[The Asia-Pacific region was home to eight of the world’s ten fastest-growing HNWI populations, led by Hong Kong (104.4%) and India (50.9%).]}

{[In India, real GDP growth increased to 6.8% in 2009 from 6.1% in 2008.]}

{[Market capitalization in India and China almost doubled]}

{{“We must create a flaunt value for diamond jewellery to realise better marginsâ€}}%%

|*Hemant Shah, Hammer Plus*|%%

In India we have so far tended to sell jewellery as an investment. We need to move away from that approach and market the product as something that is beautiful and has an emotional appeal. %%

The price which we realise must be based on the consumer perceiving it as a luxury product. %%

There are various steps we need to take to make this a reality, but none so important as a new approach to the way we understand and present ourselves and our creations. %%

For a start we must carry out widespread promotions and education about our product so that people understand how rare and valuable diamonds really are. %%

Over and above that we must work towards a situation where every piece of jewellery is easily identifiable as a brand. Of course, this is not so easy unless every jeweller develops a signature look. Presently, it is far easier for others to identify the brand that a person is wearing in the case of a watch, rather than in the case of jewellery. %%

One way of getting around this is to step up our generic promotions. By this I mean, not just emotional appeals to the consumer, but a campaign to create a specific ‘brand’ image for ALL diamond jewellery – so that anyone wearing diamonds is immediately granted recognition as a luxury consumer. %%

If we can do this successfully and all people wearing diamonds get the value of ‘flaunt’ then we can certainly expect to earn better margins. Consumers will be willing to pay more, only if they feel they are getting something additional in return. %%

We also have another USP – diamond jewellery is not only a fantastic product, it is also the only luxury product that appreciates in value over a period of time. Of course, we must be careful how we present this – it must be seen as an additional advantage, a by-product, rather than the sole or even primary USP. %%

Retailing is the second most important area that needs attention. We must convert all aspects of the buying experience into a luxury experience. We must train our sales staff and also enhance the quality of the personnel who man the shop floor. Presently with the low margins that we earn, we are unable to employ highly skilled and qualified sales personnel. This impacts the level of service we are able to provide -- as a result the consumer experience falls well short of truly luxury standards. %%

Additionally we have to improve the design and quality of the product. A piece of diamond jewellery must be perceived as something special; the consumer must be able to feel ‘I am proud to own it’. %%

Unfortunately globally we have tended to commoditise diamonds – today everyone wears them. Without impacting the breadth of the market, we must create a different image for diamonds – and this requires a serious and thoughtful process so that we can come up with innovative ideas to promote this message. %%

Finally we must realise that every successful product category in the world today is one that is able to innovate and come out with new advancements. This is something the jewellery industry really lacks – we don’t know how to innovate. %%

We have to start thinking innovatively and realise that we are selling something that is beyond the gold and diamonds that constitute the product. We must create products that stand out, are noticed and remembered. For this we need to begin spending on R & D. Manufacturers have to take a lead and invest first in creating different types of jewellery products and other studded items, products that are easily differentiated from the others in the market. And then we have to all come together and educate the consumer about this – that will make a big difference.

{{“The external environment is positive, much can be achieved with a new mindset.â€}} %%

|*Neeelesh Hundekari, Principal, A T Kearney*|%%

Jewellers are clearly a part of the luxury segment, especially the large family jewellers who have many years of tradition behind them. Currently in India there are no international brands in this space. Moreover Indians have an inherent fascination for jewellery, and this is true all across the country. So there is a definite demand for the product. %%

Diamond jewellery will be the key product in catering to the luxury segment – Indian has and always will be a gold dominated country, so relatively it is diamonds that have developed more of an image of a luxury product. %%

But there is a lot of work to be done to achieve success in this field. A few successful examples indicate that higher price points are becoming achievable as the industry modernises and undertakes promotions. %%